Apr 28, 2026•5 min read

Singapore Office Market 2026: What You Should Know

Read More

Written by: Rohan Bhattacharya

Published at: 03/10/26

Global office real estate has entered an era where intuition, legacy hierarchies, and headline numbers are no longer enough for corporate location strategy. Geopolitical shifts, digital delivery models, and the rise of Global Capability Centers (GCCs) have created a world where growth is not where it used to be, risk does not look the way it once did, and value is no longer defined purely by address.

To navigate this complexity, a more structured way of comparing markets is needed, one that moves beyond traditional rankings and instead evaluates how markets function. A Comparative Market Matrix of Growth versus Affordability offers such a lens, providing a clearer way to interpret how demand, cost, and scale interact across global office markets.

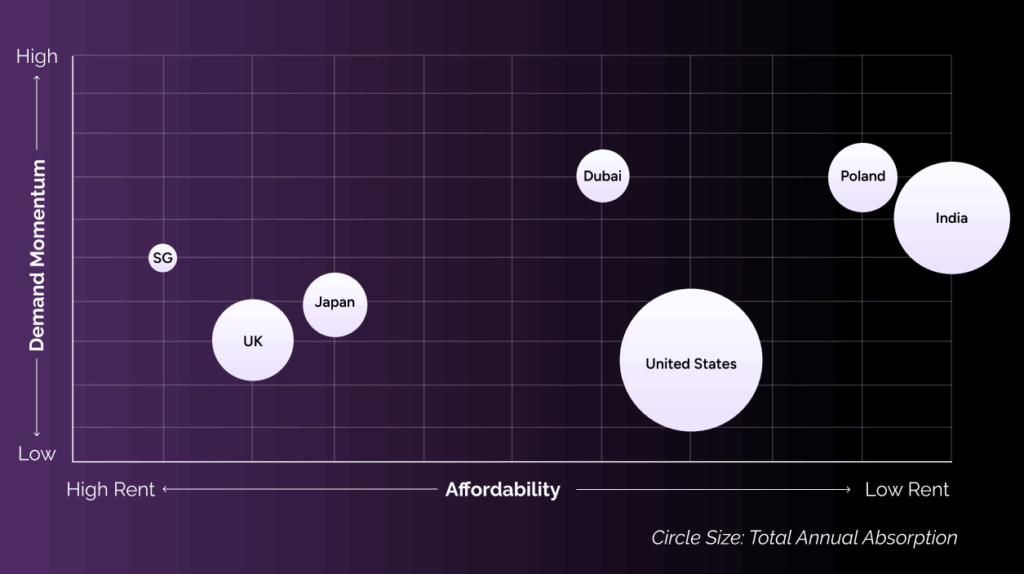

Most global real estate conversations still lean heavily on absolute numbers: total stock, total absorption, total investment volume. These metrics tell you how large a market is, but they say very little about how it behaves.

The matrix cuts through this noise by reframing comparison around momentum and affordability, two variables that matter directly to corporate strategy.

Demand momentum reflects whether a market is expanding or contracting in real time. It captures not just how much space is being leased, but how quickly space is turning over relative to total inventory.

Affordability reflects the cost of participation — a proxy for how easily a company can scale, experiment, or diversify its footprint without overcommitting capital.

Plotted together, they create a landscape of choices rather than a hierarchy of prestige.

In the high-momentum, low-cost quadrant sit markets like India and Poland.

These are not peripheral markets anymore but engines of global back-office, R&D, analytics, and shared services expansion. Their defining feature is not just cheap rent, but velocity, deals move fast, teams scale quickly, and occupiers can take large contiguous spaces without facing prohibitive costs.

India is especially unique here. It is one of the few places in the world where you can have very large buildings, very large deals, and very low rents — simultaneously. That combination is structurally rare. It is why GCCs have clustered so aggressively across Bengaluru, Hyderabad, Pune, NCR, and Chennai, reflecting the continued expansion of Global Capability Centres in India.

Poland plays a similar role in Europe: a nearshoring hub where talent, cost, and modern Grade-A supply align. Its smaller scale does not make it insignificant — it makes it nimble.

For global portfolios, these markets are best used as growth spines: places to add people, build resilience, and distribute risk away from traditional hubs.

The United States sits squarely in the mid-range of the matrix, neither truly cheap nor truly expensive, but with uneven momentum. It represents markets that are still globally dominant but internally divided.

In the U.S., prime buildings in prime cities perform well. But secondary stock struggles, vacancy is high, and overall absorption has been declining. What looks like one market is actually two: a thriving “trophy” layer and a challenged “legacy” layer.

The implication for occupiers is critical. The U.S. is no longer a blanket safe bet. It is a selective market where success depends on being in the right building in the right micro-market.

Japan and the United Kingdom sit on the opposite side of the matrix: high cost, moderate-to-low momentum, but exceptional stability.

These markets do not win on affordability or growth speed. They win on predictability.

Ultra-low vacancy in Japan and regulatory clarity in the UK create environments where risks are lower, and outcomes are more reliable. Corporations pay more, but they buy confidence: seismic resilience in Tokyo, financial depth in London, and strong governance frameworks across both countries.

These markets are not ideal for rapid headcount scaling. They are ideal for flagship presence, leadership hubs, and strategic headquarters functions.

In other words, they are the anchors of global portfolios rather than the engines.

Singapore and Dubai are fascinating precisely because they defy conventional scaling logic.

They are small in absolute absorption but extremely influential in corporate geography. Their strength lies in policy, connectivity, and concentration of high-value activity.

Singapore offers a safe, efficient gateway to Asia. Dubai provides a rapidly growing platform for MENA and global business services.

Both markets are expensive and prime-led. Both are driven heavily by relocations, renewals, and strategic positioning rather than mass expansion. Their role in global portfolios is not volume — it is control, coordination, and regional command.

If we step back, the real power of the matrix is not descriptive — it is prescriptive. It suggests that no single market should dominate a global portfolio.

A balanced strategy might look like this:

GCCs are expanding in India while keeping leadership teams in London or New York. Tech firms are distributing engineering across Poland while retaining innovation centers in Tokyo or Singapore. Financial institutions are consolidating in Dubai while running analytics out of Bengaluru.

The matrix simply makes this pattern visible and structured.

Within this global picture, India is the only market that straddles multiple advantages at once: size, momentum, affordability, and modern supply.

Unlike Poland, it has a deep geographic spread across multiple metros. Unlike the U.S., its growth is broad-based rather than concentrated only in trophy submarkets. Unlike Japan or the UK, its cost structure allows for rapid scaling. Unlike Singapore or Dubai, it has real volume.

This is why India is shifting from being seen as a “cost play” to being understood as a structural pillar of global office strategy.

Ultimately, the Comparative Market Matrix reflects a deeper transformation in how the world uses office space. We are moving from a world of prestige-led location decisions to a world of portfolio logic.

Published: March 10, 2026

Discover more insights and expert perspectives on commercial real estate and business growth

Copyright © 2026. All rights reserved.