Jun 11, 2026•5 min read

Haryana GCC Policy 2026: What the Incentives Mean for GCC Location Decisions in NCR

Read More

Written by: Vidushi Kajla

Published at: 05/04/26

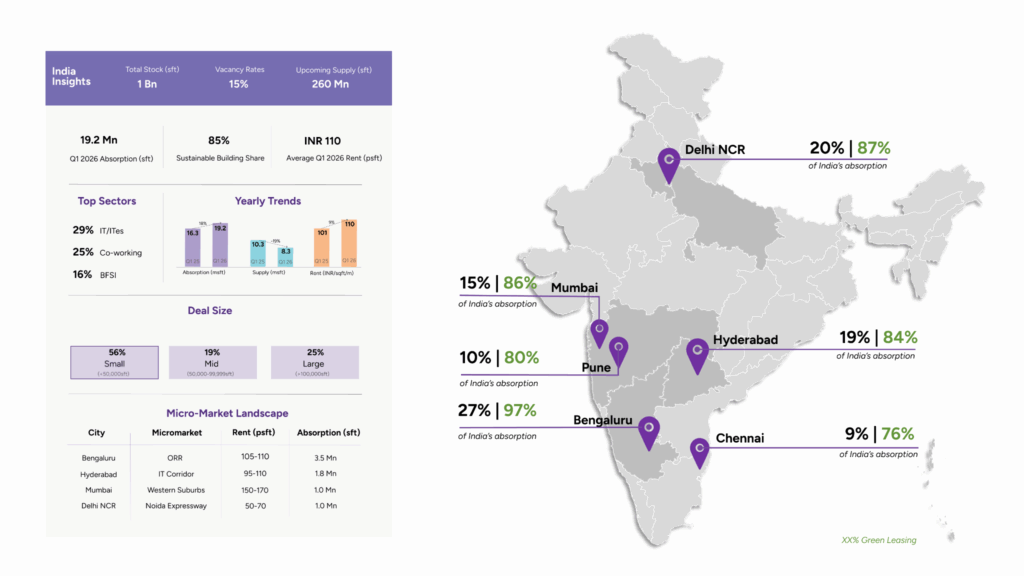

India's office market entered 2026 on a strong note, with Q1 2026 recording 19.2 million sq. ft. of gross office leasing, an approximately 18% year-on-year increase compared to Q1 2025, according to Altre's India Office Leasing Landscape Q1 2026 report. This sustained growth highlights continued occupier confidence and reinforces the structural strength of India's commercial real estate market. This analysis draws on Altre's proprietary tracking of 3,600+ commercial properties and 1,300+ coworking and managed spaces across India's top office markets.

Leasing activity remained concentrated across top metros, with Bengaluru leading at 27% share, followed by Delhi NCR (20%), Hyderabad (19%), Mumbai (15%), Pune (10%), and Chennai (9%). Unlike previous years, demand is now more evenly distributed across cities, indicating a broader-based recovery and expansion.

Average office rentals across India rose to approximately INR 110 per sq. ft. per month, marking a 9% YoY increase from INR 101 in Q1 2025. This growth reflects sustained demand for Grade-A, future-ready assets, with occupiers increasingly prioritizing quality, sustainability, and location.

On the supply side, new completions declined by approximately 19% YoY, signalling a temporary slowdown in deliveries. However, a strong pipeline of around 260 million sq. ft. of upcoming supply ensures long-term market depth.

Sectoral demand remained concentrated, led by IT/ITeS (29%), followed by co-working operators (25%) and BFSI (16%), with flexible workspace operators further strengthening their position in the leasing mix.

At the micro-market level, leasing activity remained highly corridor-driven, with key hubs such as ORR (Bengaluru), Noida Expressway (Delhi NCR), IT & Extended IT Corridors (Hyderabad), and Western & Eastern Suburbs (Mumbai) dominating absorption.

A defining trend in Q1 2026 has been the rise of flexible and managed workspaces, now accounting for a significant share of leasing activity. Co-working operators contributed 25% of total demand, highlighting occupiers'increasing preference for agile and hybrid leasing strategies.

Simultaneously, green-certified buildings have emerged as the default choice, accounting for 76–97% of leasing across major cities. These assets continue to command rental premiums, driven by global ESG mandates and occupier focus on operational efficiency and sustainability. According to the Indian Green Building Council (IGBC), India now has over 10 billion sq. ft. of registered green building footprint, a trend clearly reflected in the leasing data.

Building on Q1 trends, India's office market is expected to sustain its momentum through 2026, supported by steady demand from IT/ITeS, BFSI, and co-working operators. At the same time, occupier preferences are increasingly shifting toward high-quality, green-certified Grade-A assets, particularly within well-connected, transit-oriented micro-markets.

The growing adoption of flexible and hybrid workspace models is also set to play a key role in shaping leasing strategies, as companies move toward more agile and efficient portfolio planning. The Union Budget 2026-27 has further reinforced this trajectory through infrastructure investment, transfer pricing reforms, and dedicated support for India's services sector.

As a result, prime assets are likely to witness continued rental growth, while secondary assets may come under pressure, leading to a more pronounced gap in asset quality and pricing across the market.

Bengaluru recorded 5.1 million sq. ft. of leasing in Q1 2026, accounting for 27% of India's total absorption, maintaining its position as the top office market.

Demand was heavily concentrated along the Outer Ring Road (ORR), which alone contributed approximately 68% of city-level absorption, followed by Whitefield. The market continues to be driven by IT/ITeS occupiers (37%), along with co-working and consulting firms.

Notably, 97% of leasing occurred in green-certified buildings, highlighting the city's strong alignment with sustainability trends.

For companies evaluating Bengaluru, ORR remains the deepest Grade-A corridor, but vacancy is now sub-8%, making early engagement with available coworking and managed office inventory critical.

Delhi NCR recorded 3.8 million sq. ft. of leasing (20% share), with activity concentrated in Noida Expressway (27%) and NH-48 (18%).

Unlike other cities, demand here was led by Engineering & Manufacturing (22%), followed by IT/ITeS and co-working. Rental levels averaged around INR 120 per sq. ft., with strong traction in prime Grade-A developments.

The Engineering & Manufacturing lead in Delhi NCR is notable. It reflects the region's growing role as an operational hub, not just a services destination. Occupiers expanding in this corridor should factor in the tight supply of large floor plates along the Noida Expressway.

Hyderabad reported 3.7 million sq. ft. of leasing, contributing 19% of India's absorption, with demand split almost evenly between the IT Corridor (48%) and Extended IT Corridor (49%).

The market continues to be driven by IT/ITeS (48%) and BFSI (32%), with average rentals at INR 90 per sq. ft. Green-certified assets accounted for 84% of leasing, reinforcing occupier preference for quality spaces.

Hyderabad's near-even split between the IT Corridor and Extended IT Corridor signals that occupiers are increasingly comfortable with the expanded geography. For GCCs evaluating Hyderabad, the city offers a compelling rent-to-talent ratio, particularly for BFSI and technology functions.

Mumbai recorded 2.9 million sq. ft. of leasing (15% share), with demand concentrated in Western (37%) and Eastern Suburbs (36%).

The city remains India's most premium office market, with average rents at INR 180 per sq. ft., and significantly higher rentals in key hubs like BKC (INR 380–400 psf).

Demand was led by BFSI (23%), followed by IT/ITeS and co-working operators, with 86% of leasing in green-certified assets. Occupiers exploring alternatives to BKC should evaluate the coworking and managed office market in Mumbai's Western and Eastern Suburbs, where rental arbitrage remains significant.

Pune witnessed 2.0 million sq. ft. of leasing (10% share), with demand led by co-working operators (52%) and engineering & manufacturing (17%).

Activity remained concentrated in SBD North-East (Kharadi), which accounted for roughly 44% of absorption, supported by strong infrastructure and proximity to the airport.

Pune's co-working dominance at 52%, the highest among all cities, reflects its position as a preferred market for mid-market companies and GCC scale-up operations. Explore Pune's coworking and managed office options across Kharadi, Hinjewadi, and Baner.

Chennai recorded 1.7 million sq. ft. of leasing (9% share), with demand driven by IT/ITeS (37%) and consulting firms (25%).

Leasing activity was concentrated in Radial Road (40%) and OMR (35%), with average rentals at INR 78 per sq. ft., making it one of the most cost-effective Tier-1 markets.

At INR 78 per sq. ft., Chennai offers the lowest rental entry point among India's top six office markets, a significant advantage for cost-sensitive operations, particularly global shared services centres and GCCs optimizing for total cost of operations.

India's office market is expected to sustain its growth trajectory through 2026, supported by consistent demand from IT/ITeS, BFSI, and increasingly, co-working operators. However, the next phase of growth will be defined less by volume and more by quality, flexibility, and efficiency.

Occupiers are expected to continue consolidating into high-quality, green-certified assets, particularly within well-connected, transit-led corridors. This ongoing flight to quality is likely to drive rental appreciation in prime micro-markets, while older or non-core assets may experience continued pricing pressure.

At the same time, the rise of flexible and managed workspaces is set to reshape leasing strategies, with companies adopting more hybrid, portfolio-driven approaches to occupancy.

Overall, India's office market is transitioning into a more mature and resilient ecosystem, where demand is anchored in long-term fundamentals rather than cyclical expansion.

For a real-time view of Grade-A availability, rent benchmarks, and micro-market intelligence across these cities, explore Altre's business location advisory platform or read the full India Office Leasing Landscape Q1 2026 report.

How much office space was leased in India in Q1 2026?

India recorded 19.2 million sq. ft. of gross office leasing in Q1 2026, an approximately 18% year-on-year increase over Q1 2025, according to Altre's India Office Leasing Landscape Q1 2026 report, based on tracking of 3,600+ commercial properties.

Which city had the highest office leasing in India in Q1 2026?

Bengaluru led with a 27% share of India's total office absorption in Q1 2026, recording 5.1 million sq. ft. of leasing. Delhi NCR followed at 20%, Hyderabad at 19%, Mumbai at 15%, Pune at 10%, and Chennai at 9%.

What is the average office rent in India in 2026?

Average office rentals across India rose to approximately INR 110 per sq. ft. per month in Q1 2026, a 9% year-on-year increase. City-level rents range from INR 78 per sq. ft. in Chennai to INR 180 per sq. ft. in Mumbai, with premium hubs like BKC commanding INR 380–400 per sq. ft.

Which sectors are driving office space demand in India in 2026?

IT/ITeS led sectoral demand at 29%, followed by co-working operators at 25% and BFSI at 16%. Flexible workspace operators have significantly increased their share in the leasing mix, reflecting a broader shift toward hybrid and agile occupancy models.

What percentage of office leasing in India is in green-certified buildings?

Green-certified buildings accounted for 76% to 97% of office leasing across major Indian cities in Q1 2026, driven by global ESG mandates and occupier focus on operational efficiency. Bengaluru recorded the highest share at 97%.

What are the key office leasing corridors in India?

The most active micro-markets in Q1 2026 were ORR in Bengaluru (68% of city absorption), Noida Expressway in Delhi NCR (27%), IT and Extended IT Corridors in Hyderabad, Western and Eastern Suburbs in Mumbai, SBD North-East (Kharadi) in Pune, and Radial Road and OMR in Chennai.

Published: May 4, 2026

Discover more insights and expert perspectives on commercial real estate and business growth

Copyright © 2026. All rights reserved.