Jun 11, 2026•5 min read

Haryana GCC Policy 2026: What the Incentives Mean for GCC Location Decisions in NCR

Read More

Written by: Rohan Bhattacharya

Published at: 03/10/26

Over the last two decades, India has built one of the largest and most established Global Capability Centre (GCC) ecosystems globally. What began as a cost-efficient offshore delivery model has steadily expanded into a nationwide network of centres owning product engineering, AI/data platforms, cybersecurity, and global decision support.

By the start of 2025, India's GCC ecosystem had scaled to over 1,700 GCCs and 2,700+ operating units, reflecting both depth and diversification. Technology and IT-led GCCs continued to dominate with a ~40% share, while BFSI, engineering, healthcare, and consulting together formed a strong secondary layer of demand. Bengaluru (31%) remained the primary hubs, followed by Delhi NCR, Mumbai, Hyderabad, Pune, and Chennai, while Tier-2 cities began registering early yet meaningful traction.

By 2025, India's GCC market reflected maturity. Activity was no longer limited to a single city or a narrow set of functions. GCCs started spreading across multiple metros, supported by deep talent pools, established office markets, and a growing base of experienced operators.

The trend seen in 2025 is one of steady, broad-based growth. New setups and expansions occurred in parallel, across Tier-1 cities and select Tier-2 locations, indicating that global firms are not only entering India but also increasing their footprint over time. Sector participation has also widened, with technology remaining central while engineering, BFSI, healthcare, retail, and consulting continue to add capacity.

Overall, the 2025 data positions India as a stable, large-scale GCC market with geographic depth, sector diversity, and sustained engagement from global enterprises.

In 2025, India recorded 170+ GCC setups, accounting for over 23 million sq ft of office absorption. The split between new GCCs (85+) and expansions (80+) was nearly even, highlighting that growth is coming from both fresh market entry and capacity scaling within existing centres.

This balance indicates that India is no longer just an entry market but also a scale market for mature global operations.

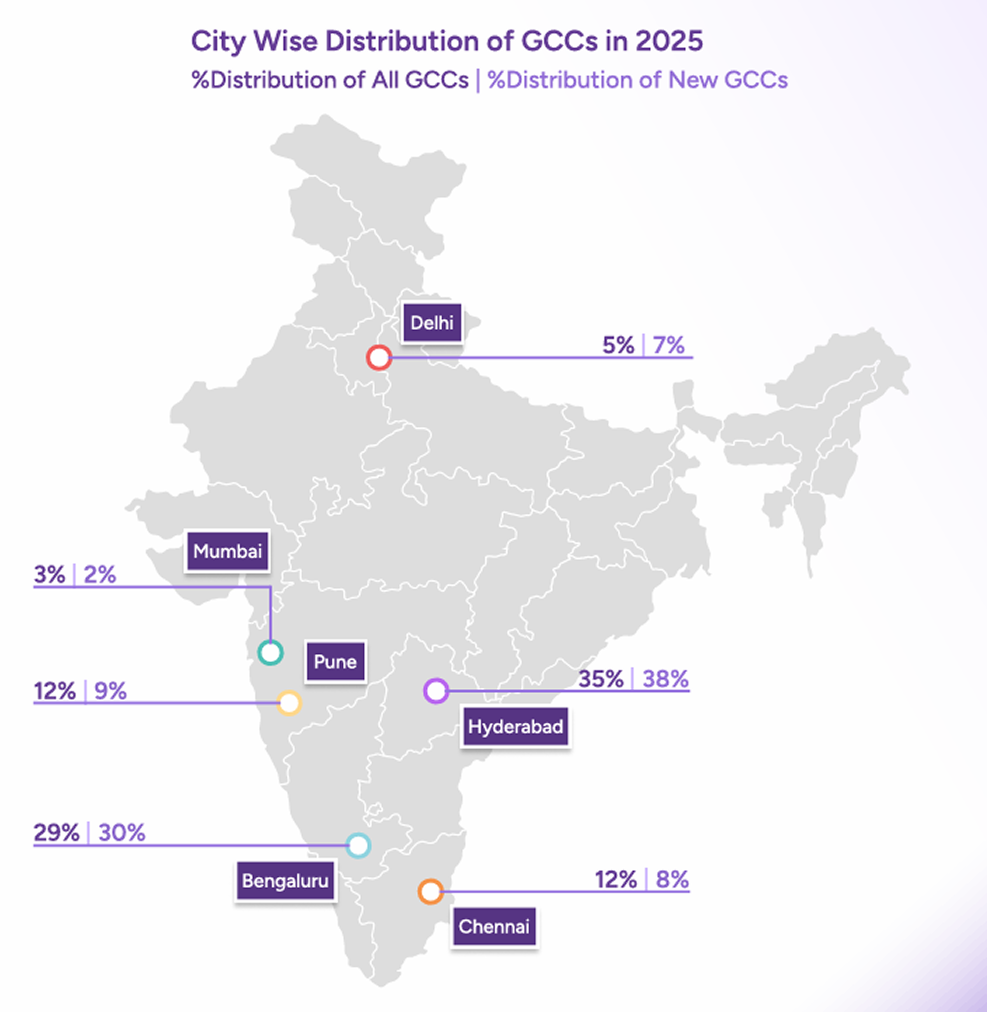

City-level distribution: broad-based, not single-city dependent

GCC activity in 2025 was spread across all major office markets, while Hyderabad emerged as the largest contributor in terms of overall activity, while Bengaluru remained the largest contributor; other cities continued to play defined roles in expansion and sector-specific growth.

Pune and Chennai recorded a high number of expansion-led transactions, reinforcing their position as stable scale-up markets.

Mumbai remained relevant primarily for BFSI-led GCCs.

Delhi NCR saw relatively fewer transactions but remained active, with a noticeable preference for managed and flexible office formats.

Tier-2 cities, though still small in absolute numbers, recorded new GCC additions, signalling early-stage diversification beyond Tier-1 hubs.

Overall, the data indicates that GCC demand in India is multi-city in nature, rather than concentrated in one or two locations.

The United States continued to dominate as the primary source of GCC setups, accounting for approximately 65% of total activity, followed by EMEA (~25%) and APAC (~10%). While the US remains the largest contributor at a national level, the city-wise mix varied.

Bengaluru and Hyderabad remained more US-skewed, reflecting their strong alignment with technology- and platform-led mandates. In contrast, engineering- and manufacturing-led cities such as Chennai and Pune showed a more balanced mix of US, EMEA, and APAC-origin firms. Delhi NCR stood out for its relatively higher APAC participation, indicating a more diversified source profile compared to other major markets.

This distribution points to a gradual broadening of India's GCC source markets across cities, rather than uniform dependence on a single geography.

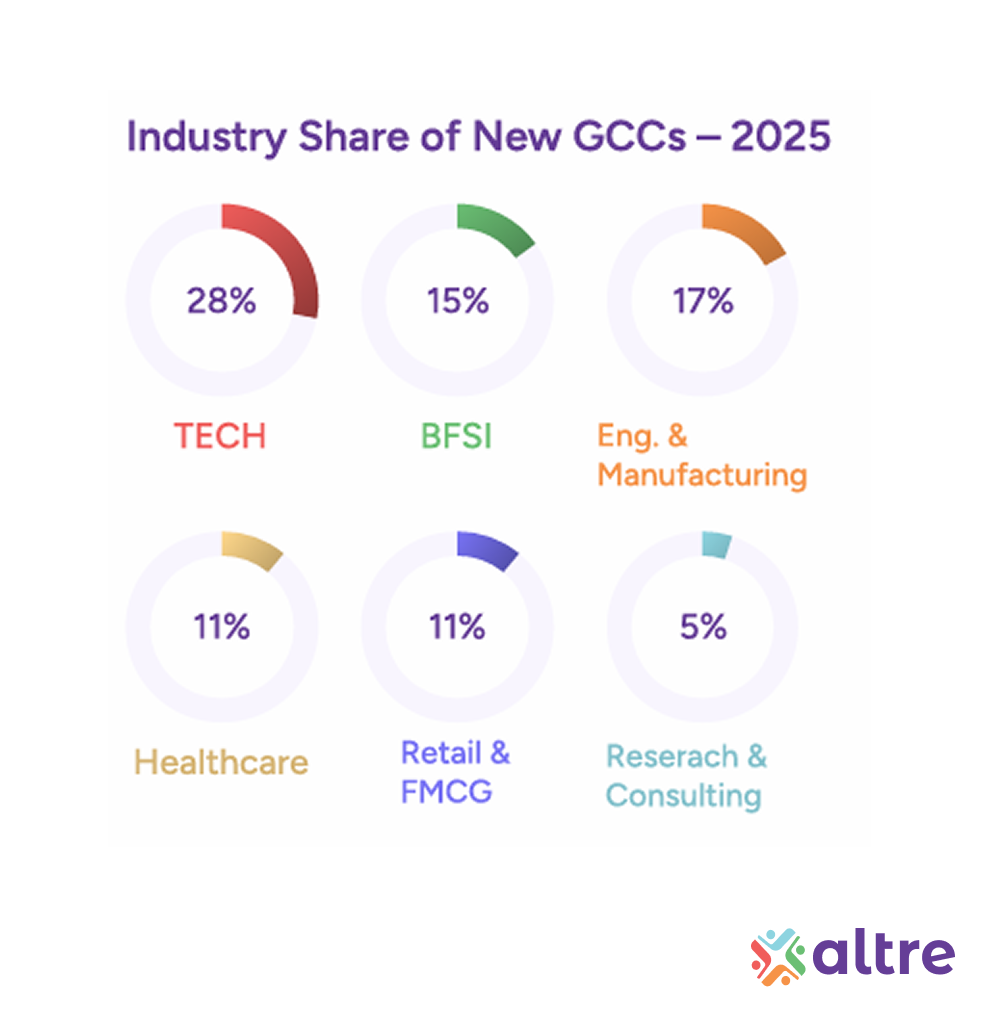

Industry mix: technology-led but increasingly diversified

GCC setups in 2025 were led by technology and digital-heavy sectors, but activity extended across a wide range of industries.

This distribution shows that while technology remains the largest driver, non-tech sectors are increasingly establishing GCCs with technology, data, and platform-oriented mandates.

In 2025, the policy environment around GCCs continued to strengthen at both the state and national levels. Companies evaluating GCC expansion in India increasingly require data-driven location advisory covering talent availability, real estate supply, and operating costs but additionally region-specific policies as well. Several states, including Gujarat, Maharashtra, Madhya Pradesh, Uttar Pradesh, and Odisha, either introduced new GCC-focused policies or enhanced existing ones, with an emphasis on simplifying operational processes, offering targeted incentives for new setups, and encouraging GCC development beyond established Tier-1 markets.

States such as Tamil Nadu, Uttar Pradesh, Maharashtra, and Gujarat provide direct salary reimbursements and hiring-linked incentives, significantly reducing long-term people costs. This is complemented by strong innovation support through Centres of Excellence, R&D grants, and patent funding, particularly in states like Uttar Pradesh, Madhya Pradesh, Gujarat, and Maharashtra, enabling GCCs to move beyond execution into high-value engineering and product development. On the cost side, power, cloud, and utility subsidies across key states further enhance operating efficiency, with several offering multi-year electricity duty exemptions and capped reimbursements. Collectively, these benefits make Maharashtra and Uttar Pradesh attractive for large-scale operations, Tamil Nadu and Karnataka ideal for tech-led GCCs, and Madhya Pradesh and Rajasthan highly competitive for cost-sensitive expansions, reinforcing India's position as a structurally advantaged GCC destination over the long term.

Alongside this, industry bodies at the national level advocated for a more structured and standardized GCC framework, particularly around taxation and compliance, helping reduce ambiguity for global enterprises evaluating India. Together, these measures contributed to a more supportive ecosystem and helped sustain the pace of new GCC additions during the year.

Hiring patterns across GCCs in 2025 showed increased demand for:

In parallel, GCCs increasingly operated as integrated global teams, rather than standalone support units. Cross-location collaboration and shared ownership of global functions became more common.

Based purely on market data:

The 2025 GCC landscape reflects measured, sustainable growth, rather than short-term spikes. As GCCs scale operations, office space strategy for GCCs increasingly requires a balance between talent clusters, cost efficiency, and future expansion capacity. AI-driven workspace advisory tools are also helping occupiers evaluate cities, supply pipelines, and talent availability before committing to large-scale GCC setups.

The consistency across cities, industries, and source markets suggests that India's GCC ecosystem has moved into a mature phase, where expansion decisions are driven by operating requirements rather than experimentation.

For stakeholders like occupiers, developers, and policymakers, the data points to a GCC market that is stable, diversified, and nationally distributed, with clear leaders but no single point of dependence.

Published: March 10, 2026

Discover more insights and expert perspectives on commercial real estate and business growth

Copyright © 2026. All rights reserved.